Why insurance coverage for treatment matters

When you are considering treatment, it is natural to worry about how much it will cost and what your health plan will actually pay. Understanding your insurance coverage for treatment helps you make decisions based on facts instead of fear. It also gives you more control over where you go, how long you stay, and which services you receive.

Health insurance coverage means that your plan will pay for some or all of the cost of a covered service, medication, or item. These covered services are often referred to as benefits or covered benefits [1]. When you know what your benefits are, you can approach admissions and care planning with more confidence.

If you are just starting to explore help, you might find it useful to review the general steps in the rehab intake process and admissions for rehab as you read through this guide.

Understanding the basics of insurance coverage

Before you look at specific programs or costs, it helps to understand some core terms that affect how your insurance coverage for treatment works in practice.

How coverage and networks work

Every health plan has a list of services it covers and a network of preferred providers. Plans usually pay a higher share of the bill when you use in‑network providers. If you choose an out‑of‑network provider, you can face higher out‑of‑pocket costs or even be responsible for the full amount [1].

In simple terms, networks matter because they directly influence:

- How much of the bill your plan pays

- How much you pay out of pocket

- Whether preauthorization or referrals are needed

If you are considering a private rehab facility, asking whether it is in network with your specific plan is one of the most important early questions.

Deductibles, copays, and out‑of‑pocket limits

Most insurance plans use cost sharing. This means you and your plan each pay part of the cost of covered services. According to the Texas Department of Insurance, you typically share costs through premiums, deductibles, copayments, and coinsurance, and federal law sets an annual limit on your out‑of‑pocket expenses. Once you reach that limit, your plan must cover 100 percent of covered costs for the rest of the year, not including premiums [2].

In practical terms for treatment:

- Your deductible is the amount you must pay before your plan starts paying a larger share.

- Copays are fixed amounts you pay for specific visits or days of care.

- Coinsurance is a percentage of the cost of care that you pay once the deductible is met.

Knowing where you stand with your deductible and out‑of‑pocket maximum can help you estimate what a stay in treatment will actually cost you.

Essential health benefits and behavioral health

Federal law requires most individual and small‑employer plans to cover 10 categories of essential health benefits, which include mental health and substance use disorder services and many preventive services at no extra cost when you use in‑network providers [2]. For you, this means that treatment for addiction or co‑occurring mental health conditions is not considered optional. It is a core part of what many plans are required to cover.

In addition, plans cannot deny you coverage or raise your premiums solely because of preexisting conditions. Insurers also cannot cancel your policy except in cases of fraud or intentional misrepresentation, and they must allow you to renew individual coverage regardless of your health status [2].

Verifying your insurance before you start

Once you understand the basics, the next step is to confirm exactly how your insurance coverage for treatment will apply to the program you are considering. This process is called insurance verification or insurance eligibility verification.

Why verification is so important

Insurance verification means confirming in advance what your health plan will pay for and what your financial responsibility will be [3]. Taking a few minutes to verify coverage can help you avoid:

- Unexpected medical bills

- Denied services that you thought were covered

- Delays in starting or continuing treatment

For medical practices, proper eligibility verification helps reduce claim denials and billing errors, and it supports faster reimbursements and clearer communication of your costs [4].

From your perspective, verification is about peace of mind. When you verify your benefits before admission, you know:

- Whether your insurance is active

- Which levels of care are covered

- If prior authorization is required

- What your copays, deductibles, and coinsurance will be

If you would like help with this step, you can use tools that allow you to verify insurance for treatment directly with a rehab provider.

How the verification process works

The insurance eligibility verification process usually includes three main steps [4]:

-

Collecting your information

You provide your full name, date of birth, policy or member ID, group number, and insurance company details. You may also be asked about your employer and the primary account holder. -

Confirming benefits with the insurer

The provider or admissions team contacts your insurance company, often through real‑time electronic tools, to confirm that your coverage is active and to review your behavioral health benefits. They check for coverage limits, in‑network requirements, and any preauthorization or referral rules. -

Communicating results to you

Once verification is complete, the team will review your expected coverage for treatment, including any copays, coinsurance, or amounts applied to your deductible. This gives you a clear picture before you decide on admission.

Many providers use electronic verification tools that can return information quickly and accurately. This real‑time access can help reduce delays and errors in confirming coverage [4].

Using your insurer’s tools

Most insurance companies now offer online accounts that show coverage in detail. HealthPartners, for example, recommends that members sign into their online account to view benefits, in‑network deductibles, coverage levels, out‑of‑pocket limits, and any requirements for prior authorization [1].

You can usually also:

- Review your Summary of Benefits and Coverage (SBC), which outlines what your plan covers and how costs are shared [1]

- Use cost estimator tools to estimate out‑of‑pocket costs for different treatments and providers [1]

These tools can be used alongside the provider’s own verification process to give you the most complete picture possible.

Connecting coverage to real treatment options

Once you understand your benefits and have verified your insurance coverage for treatment, you can begin to compare specific options with more clarity. This is where questions about cost, amenities, and privacy become real considerations in your choice.

In‑network vs out‑of‑network programs

In‑network programs usually result in lower costs because your plan has negotiated rates with those providers. Out‑of‑network programs may still be covered to some degree, depending on your plan, but often with higher deductibles or coinsurance.

If you are looking at a private rehab facility that offers features like private rooms and a more intimate setting, it is important to ask:

- Are you in network with my insurance plan?

- If not, does my plan offer any out‑of‑network benefits for residential treatment?

- Can you help me estimate my out‑of‑pocket cost for a typical stay?

Many clients are surprised to learn that their insurance will pay a significant portion of treatment even at private facilities that focus on comfort and privacy.

Cost transparency and what to ask

Cost transparency means that you receive clear, written information about what treatment is likely to cost before you commit to admission. When you talk with an admissions team, you can ask specific questions such as:

- What is the daily or weekly rate for the level of care I am considering?

- How much of that does my insurance typically cover for someone with my plan?

- What fees are not covered by insurance, such as specialized assessments or optional services?

- How do you handle situations where my insurance coverage changes during treatment?

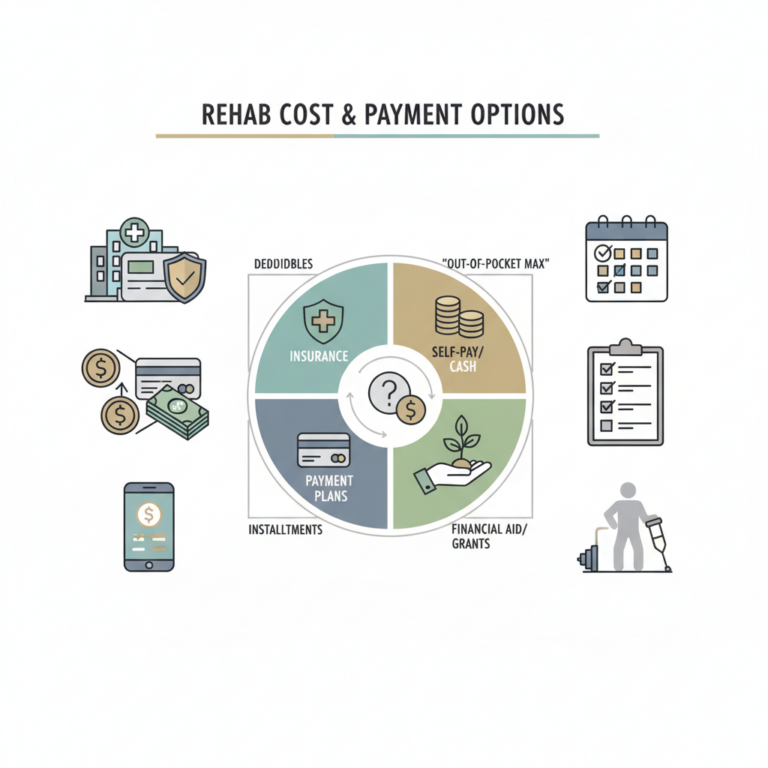

Exploring resources on rehab cost and payment options can help you prepare these questions and understand how facilities typically structure their fees.

Private rooms, comfort, and clinical care

Privacy and comfort can strongly influence how safe and focused you feel during treatment. Many private programs offer single‑occupancy rooms, quiet common areas, and amenities that support rest and reflection. It is understandable to wonder whether your insurance will cover treatment in a setting like this.

In most cases, insurance does not pay extra because a room is private. Instead, it pays for the covered level of care, such as residential treatment or intensive outpatient services, based on medical necessity and your benefits. The provider then decides how to structure the environment. This means you may be able to access private rooms and a more comfortable setting without paying the full cost out of pocket.

If you are comparing facilities, you might find it helpful to tour residential rehab, either in person or virtually, so that you can see how the environment, privacy, and clinical services align with what your insurance will support.

When you combine a clear understanding of your insurance coverage with a transparent provider, you can focus less on financial uncertainty and more on your actual recovery.

Planning your share of the cost

Even with strong insurance coverage for treatment, you will usually have some financial responsibility. Planning for your share in advance can reduce stress and help you stay focused on your goals.

Estimating your out‑of‑pocket costs

Several pieces of information come together to determine what you are likely to pay:

- Your current deductible status

- Your coinsurance rates for inpatient or outpatient behavioral health services

- Any daily copays for residential or intensive outpatient care

- Whether the facility is in network

Using your insurer’s cost estimator tools can give you a starting estimate [1]. The provider’s admissions or billing team can then refine that estimate based on their usual charges and your specific plan.

You can also discuss payment approaches such as:

- Paying your estimated share monthly during treatment

- Setting up a post‑discharge payment plan

- Coordinating with family members who may be supporting you financially

Exploring options for financing rehab programs can give you a sense of how others structure payments when insurance does not cover everything.

Using a Health Savings Account (HSA)

If you have an HSA, these funds can often be used for many treatment‑related expenses that qualify as eligible medical costs. Verifying your coverage in advance helps you use HSA dollars wisely, since you can confirm which services are covered and then decide whether to spend or save your HSA balance for future care [3].

This planning can be especially helpful when:

- Your deductible is high and you want to use HSA funds to meet it

- You expect ongoing outpatient care after residential treatment

- You want to avoid depleting your HSA on services that could have been covered differently

Special situations and protections

In some cases, you may run into issues such as disputed charges, surprise bills, or questions about whether your plan followed the rules. It is important to know that there are protections available to you.

Surprise billing and balance billing protections

Balance billing happens when a provider bills you for the difference between what your insurer pays and what the provider charges. Under Texas and federal laws, balance billing was banned in certain emergency situations and cases where you had no choice of provider for services between January 1, 2020 and December 31, 2021 [5]. Starting January 1, 2022, protections were expanded to include air ambulance services in addition to covered emergency care and some situations where you had no choice of doctors [5].

If you receive a balance bill that does not seem consistent with these protections, the Texas Department of Insurance offers guidance on how to get help with a surprise medical bill [5].

When you need to file a complaint

If you believe your insurer did not follow the terms of your policy or applicable law, you can sometimes file a complaint with your state’s insurance department. In Texas, the Department of Insurance can help with issues involving companies and health plans that it regulates, although many employer plans and federal programs like Medicare are not under its authority [5].

To file a complaint with the Texas Department of Insurance, you must sign a consent form that allows them to share your complaint information with the company or person involved. Without this consent, they might not be able to assist you [5].

Understanding these options can give you confidence that you have recourse if you encounter a problem with coverage for your treatment.

If you have Medicare coverage

If you are covered by Medicare and are receiving treatment, there are specific rules for claims. Medicare generally requires that claims be filed within 12 months of the service date. If the claim is not filed on time, Medicare will not pay its share unless an exception applies [6].

If a provider refuses to file the claim and you pay out of pocket, you may submit your own claim using the Patient Request for Medical Payment form (CMS‑1490S), which is available in English and Spanish [6]. You can also check the status of Medicare claims through your Medicare Summary Notice, your secure online Medicare account, or your plan’s statements [6].

Taking your next step with confidence

Navigating insurance coverage for treatment can feel complex, but you do not have to sort through it alone. When you combine a clear understanding of your benefits with support from an experienced admissions team, the process becomes more manageable.

You can move forward by:

- Checking whether your preferred program is an insurance accepted rehab

- Asking the admissions team to verify insurance for treatment and explain your benefits in everyday language

- Reviewing rehab cost and payment options to plan for your share of costs

- Exploring a private rehab facility and possibly scheduling a tour residential rehab to see the environment firsthand

Most importantly, remember that health care coverage exists to help you get needed care and protect you from the full financial impact of serious illness or injury [2]. Understanding how your coverage works is not just about numbers. It is about giving yourself a stable foundation so that you can focus on what matters most, your recovery and long‑term wellbeing.