How insurance accepted rehab works

When you start searching for “insurance accepted rehab,” you are often trying to answer one urgent question: can you actually afford treatment. The good news is that most modern health plans are required to cover substance use and mental health care at levels similar to medical care, although the fine print of your policy will determine how much you pay out of pocket [1].

Private insurance, Medicare, and Medicaid all cover some form of addiction treatment. What varies is the type of services covered, how long you can stay, and which facilities are in network. Understanding these pieces helps you use your benefits fully and avoid surprise bills.

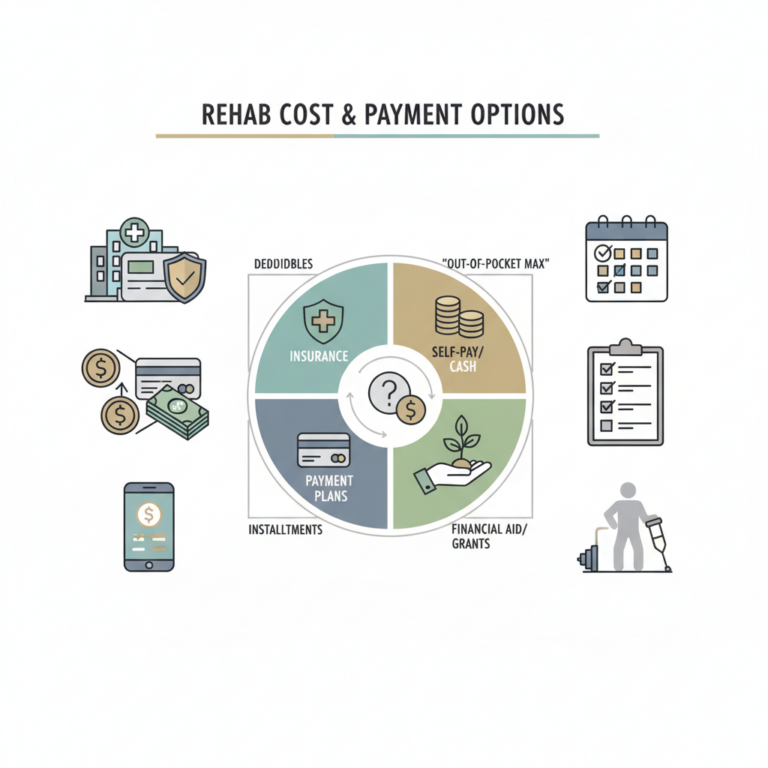

In many cases, admissions teams can check your benefits before you commit to a program so you know what is covered and what your share of the cost will be. You can also review common rehab cost and payment options while you compare facilities.

Why most plans now cover rehab

Modern coverage for “insurance accepted rehab” did not happen by accident. Several laws reshaped how insurers handle addiction and mental health treatment, and these protections work in your favor.

Parity and essential health benefits

Two major protections are important for you to know:

- The Mental Health Parity and Addiction Equity Act requires that when a plan offers behavioral health benefits, the financial requirements and treatment limits cannot be more restrictive than for medical or surgical care. In other words, an insurer cannot set dramatically higher copays or tighter visit limits just because the service is for addiction treatment [2].

- The Affordable Care Act requires new individual and small group plans to cover mental health and substance use disorder services as essential health benefits, with coverage levels comparable to other medical care [3].

These rules do not mean that everything is free, but they do mean that addiction treatment is no longer treated as an optional extra. Your plan will still have deductibles, coinsurance, and networks, but it must treat behavioral health in a similar way to physical health.

Why this matters for access

Even with these protections, most people who need help are still not in treatment. In 2021 more than 46 million Americans aged 12 or older had a substance use disorder, but about 94 percent did not receive care, often because of concern about cost [3]. In 2024 only about 19.3 percent of people who needed substance use treatment actually received it [4].

Understanding that your insurance is required to support addiction treatment, and learning how to use your benefits, can help you move from hesitation to action.

Types of insurance that may cover rehab

Different insurance paths can help you access an insurance accepted rehab program. The details vary, but several broad categories are common.

Private health insurance

Most private health insurance plans from major carriers such as Blue Cross Blue Shield, Aetna, UnitedHealthcare, Cigna, Humana, and Anthem typically include coverage for inpatient and outpatient substance use treatment [5].

With private insurance you can expect:

- Coverage for inpatient rehab, residential rehab, partial hospitalization, intensive outpatient, and outpatient therapy, as long as these levels of care are medically necessary

- Different benefit levels for in network versus out of network facilities

- A requirement for preauthorization or clinical review in many cases

Most rehab centers that work with private insurance employ specialists to help you understand your coverage, verify benefits, and explain any out of pocket responsibilities [5].

Employer coverage and COBRA

If you recently lost a job that included health benefits, you might still be able to use that coverage for rehab through COBRA. COBRA lets you continue your previous employer plan for a period of time, as long as you pay the full premium.

Treatment providers often accept COBRA coverage and may ask for a copy of your COBRA election form during intake [4]. This can be a bridge that allows you to attend residential or inpatient care while you stabilize.

Medicare

If you qualify for Medicare, different parts of your coverage may support addiction treatment:

- Medicare Part A can cover medically necessary inpatient hospital care for drug and alcohol rehabilitation, including room and board, nursing, therapy, and medications, as long as the stay is documented as medically necessary. There is no fixed lifetime limit on treatment length, but standard Medicare benefit periods and deductibles still apply [2].

- Medicare Part B can cover outpatient counseling, partial hospitalization, and some physician services related to addiction treatment.

- Medicare Part D can cover certain medications used in alcohol treatment, although some drugs such as methadone may be excluded [3].

If you rely on Medicare, you will want to confirm whether a facility is approved to bill Medicare and which services they provide under that coverage.

Medicaid

Medicaid, a joint federal and state program, covers inpatient and other addiction treatment services in every state, but the type and length of coverage varies by state and by your personal eligibility [2]. Some states fund residential treatment, while others emphasize outpatient and community based care.

If you are uninsured or underinsured and meet income or disability criteria, Medicaid can provide a path into treatment that does not depend on employment.

Veterans benefits and TRICARE

If you are a veteran or an active duty service member, you may have access to substance use treatment coverage through:

- The U.S. Department of Veterans Affairs, which offers a range of addiction treatment services and can coordinate with community providers. Some private treatment organizations work directly with the VA and employ Veteran Liaisons to help you navigate benefits and choose a level of care [4].

- TRICARE, which often covers at least some costs of alcohol and drug rehab for eligible service members and families [3].

If you have VA or TRICARE benefits, it can be helpful to ask a facility if they have dedicated staff who regularly work with these systems.

What “insurance accepted” usually covers

“Insurance accepted rehab” often sounds like a simple promise, but what is actually covered for you depends on your plan. Still, most insurers handle certain categories of services in fairly predictable ways.

Common levels of care

Depending on your clinical needs, your plan may cover some or all of these levels of care:

- Medical detoxification in a supervised setting

- Inpatient or residential rehab, often with 24/7 support and structured programming

- Partial hospitalization programs, with several hours of care most days of the week

- Intensive outpatient programs

- Standard outpatient counseling and medication management

Facilities like The Plymouth House, for example, use your insurance information to determine whether your plan will support medical detox and subsequent residential care, and sometimes coverage may reach up to 100 percent of treatment costs if your benefits are strong and the facility is in network [6].

Services within a rehab stay

Within an approved level of care, plans typically cover:

- Clinical assessments and treatment planning

- Individual and group therapy sessions

- Family therapy, where appropriate

- Medication management

- Nursing and physician oversight for medical needs

- Some complementary or holistic services when they are part of a bundled daily rate

Your plan may not separately list each component, especially in a private rehab setting that bills a daily or per stay rate. If private rooms, amenities, or certain experiential therapies are part of a standard daily charge for an in network private rehab facility, they may effectively be included in what your insurance pays. In other cases, you might pay a higher share if you choose upgraded accommodations.

What may not be covered

Every policy is different, but you should be prepared for limits around:

- Luxury amenities that are not tied to medical necessity

- Extended stays beyond what the insurer considers clinically necessary

- Certain out of network providers or services

- Long term sober living that is not classified as treatment

Talking through these details with an admissions specialist before you arrive is the best way to avoid financial surprises.

How admissions and verification typically work

When you contact an insurance accepted rehab, one of the first steps is usually an insurance verification. This is part of the overall rehab intake process and sets expectations for both care and cost.

Step 1: Initial phone call and screening

You typically start with a phone call to admissions. During this call, staff will:

- Ask about substances used, history, and any co occurring conditions

- Discuss your current safety and any urgent medical issues

- Gather your insurance information including carrier, member ID, and group number

This conversation is not a commitment to attend. It is a chance for you to ask questions, including whether the facility offers private rooms, what a typical day looks like, and how families are involved.

Step 2: Insurance benefits check

Most rehab centers that accept insurance will then:

- Contact your insurer to verify that your policy is active

- Confirm what addiction treatment benefits you have

- Determine your deductible status, copays, and coinsurance

- Ask about prior authorization requirements and any length of stay guidelines

Facilities often perform this benefits check at no cost to you. Admissions specialists handle the back and forth with insurers, secure preauthorizations, and may help with appeals if coverage is initially denied [2].

Organizations such as The Plymouth House integrate this verification directly into their admissions process so that before you enter treatment, you understand coverage levels and estimated out of pocket costs [6].

Step 3: Clinical review and approval

Your insurer may require a clinical assessment to determine medical necessity. This can happen over the phone or through documentation submitted by the facility. The goal is to match you with the right level of care, such as:

- Inpatient detox if you are at risk of severe withdrawal

- Residential treatment if you need a structured 24/7 environment

- Intensive outpatient if you can remain at home with strong support

Once medical necessity is confirmed, approval is granted for an initial period of stay. During your time in treatment, the facility usually communicates with the insurer to request extensions when clinically appropriate.

Step 4: Finalizing your admission

After benefits are verified and care is authorized, staff will:

- Review your expected costs, payment schedule, and any deposit

- Outline logistics such as arrival time and what to pack

- Clarify room options, including availability of private rooms if that is important to you

- Answer questions about program structure, safety, and confidentiality

If you have questions about other financial resources, you can also explore financing rehab programs and payment plans at this stage.

You have the right to know in advance how your insurance will be used, what your estimated out of pocket costs are, and what treatment options are available to you.

Balancing cost, comfort, and clinical care

When you compare insurance accepted rehab programs, you are usually weighing two things at once: what your insurance will pay for and where you will feel safe and supported enough to do the hard work of recovery.

In network versus out of network

Insurers typically pay more of the cost when you choose an in network provider. However, in some situations an out of network facility may be the best fit for your needs. For example, you might choose a center that:

- Specializes in your specific substance or co occurring condition

- Offers a smaller, more private setting or more individualized care

- Provides private or low occupancy rooms that help you rest and focus

You can ask a facility whether they are in network or out of network with your plan, and you can also ask your insurer for a list of participating rehab providers. Some facilities will still work with out of network benefits and help you submit claims.

Private rooms and amenities

Private rooms are a priority for many people who are already feeling vulnerable. While some insurance plans reimburse the same daily rate regardless of room type, others distinguish between standard and upgraded accommodations.

When you tour or virtually tour residential rehab, you can ask:

- Are private rooms standard or an optional upgrade

- Does insurance reimburse the same amount regardless of room type

- If there is an upgrade cost, how much is it per day and what is included

Understanding how private rooms fit into the fee structure helps you decide what is most important for your comfort and healing.

Transparency around costs

Clear information reduces anxiety during an already stressful time. Before you decide on a program, you are entitled to:

- A written estimate of your total cost of care

- A breakdown of what your insurance is expected to pay

- An explanation of how changes in length of stay might affect your costs

You can also refer to resources on insurance coverage for treatment and rehab cost and payment options to prepare questions for admissions.

Options when you have limited or no insurance

Insurance accepted rehab is only one route into treatment. If your coverage is limited, or if you are uninsured, there are still ways to access help.

State funded and low cost programs

State funded treatment centers provide free or low cost rehab for people who cannot afford private care or who have inadequate insurance. These programs are an important safety net for both insured and uninsured individuals [4].

If you qualify, you might have access to:

- Residential or outpatient addiction treatment

- Medication assisted treatment

- Case management and recovery support services

Availability and wait times vary by state and region, so it is helpful to start this process as early as you can.

Using Medicaid, marketplace plans, or new coverage

If you are uninsured, you might still be able to:

- Apply for Medicaid if you meet income or disability criteria

- Enroll in a plan through your state or federal health insurance marketplace, where all plans must include substance use and mental health benefits [3]

Some facilities can connect you with navigators who help you start these applications, especially if enrollment will allow you to access a higher level of care.

SAMHSA’s National Helpline

If you are not sure where to begin, you can contact SAMHSA’s National Helpline, a free and confidential service available 24 hours a day in English and Spanish. Callers receive information and referrals to:

- Local treatment facilities

- Support groups

- State funded programs and sliding scale providers

The helpline can also direct you to state offices that oversee public treatment options for people who are uninsured or underinsured, and to facilities that accept Medicare or Medicaid [7]. While the service does not provide counseling, trained information specialists can help you move from confusion toward concrete next steps. In 2020 the helpline received more than 833,000 calls, a 27 percent increase from the year before, which reflects how many people rely on it to find treatment [7].

Questions to ask before you commit

As you research insurance accepted rehab options, it can help to use a simple framework when you talk with admissions teams or review program materials.

- Coverage and cost

- Is my plan in network or out of network with your facility

- What is my estimated out of pocket cost for the full recommended stay

- How do private rooms or upgraded amenities affect cost, if at all

- Do you offer payment plans or other financing rehab programs

- Clinical fit

- What levels of care do you offer and which one are you recommending for me

- How do you handle co occurring mental health conditions

- What does a typical day of treatment look like

- Environment and privacy

- Are private rooms available and how many people share common spaces

- How do you ensure safety and confidentiality

- Can I tour the facility in person or online before admission, perhaps through a tour residential rehab option

- Logistics and support

- How quickly can I be admitted once insurance is verified

- What does your rehab intake process include

- How do you involve family or support systems in care

Using these questions helps you balance financial realities with the quality of care and environment you need.

Taking your next step toward treatment

Insurance accepted rehab exists to make high quality addiction treatment more accessible. Most private plans, Medicare, and Medicaid now cover significant portions of inpatient or residential rehab, and many facilities work directly with insurers to verify benefits and reduce your administrative burden [8].

If you are ready to explore treatment:

- Gather your insurance card and any recent statements

- Reach out to admissions teams and ask them to verify your benefits

- Use resources on verify insurance for treatment and admissions for rehab to understand what to expect

You do not have to decode your coverage alone. With the right information and support, you can find a program that accepts your insurance, is transparent about costs, and offers a safe, comfortable environment, including private rooms where available, so you can focus on recovery.